Leaving or Returning to the UK

UK Tax When You Leave the United Kingdom: Rates, Forms and the Residence Tests

Leaving the UK, or coming back after time abroad, raises real tax questions across income tax, dividends, self-employment, capital gains and residence. Poor planning can mean unexpected bills, missed reliefs or double tax. This guide covers your residence status under the Statutory Residence Test, the rates and forms, split-year treatment, capital gains on return, and the tools to estimate your position.

The essentials

- ✓ Your liability turns on whether you are UK resident under the Statutory Residence Test.

- ✓ Leave mid-year and split-year treatment may tax only the UK part on worldwide income.

- ✓ As a non-resident you generally pay UK tax only on UK-source income (rent, pensions, UK company dividends).

- ✓ Return within 5 tax years and the temporary non-residence rules can pull gains back into UK CGT.

- ✓ Tell HMRC you have left using Form P85, or the SA109 residence pages if you file Self Assessment.

Why people leave the UK

Comprehensive data purely on tax-driven departures is limited, but the context is telling. The UK’s net migration reached about 906,000 in the year ending June 2023. The Tax Justice Network reports that claims of a mass non-dom exodus are exaggerated, with HMRC data showing departures in line with expectations. A separate survey found 21% of respondents said higher taxes had prompted them to consider cutting ties with the UK. Not every move is tax-driven, but tax is increasingly part of the decision.

Residence status: the Statutory Residence Test

Under the SRT (in force from 6 April 2013) you test residence for each tax year in a set order: first the automatic overseas tests (meet one and you are non-resident), then the automatic UK tests (meet one, with no overseas test met, and you are resident), and only if neither applies, the sufficient ties test. Days are counted on the midnight rule: present in the UK at midnight counts as a UK day.

Automatic UK residence tests

| Test | Requirement |

|---|---|

| UK test 1 | You are present in the UK for 183 days or more in the tax year. |

| UK test 2 | You have a UK home for at least 91 consecutive days (30 of them in the tax year), are present there on at least 30 days in the year, and have no overseas home (or use any overseas home fewer than 30 days). |

| UK test 3 | You work full-time in the UK (averaging at least 35 hours a week) over a 365-day period, more than 75% of working days in the UK, with at least one such day in the tax year. |

Automatic overseas (non-residence) tests

| Test | Requirement |

|---|---|

| Overseas test 1 | UK resident in one or more of the previous three tax years, and you spend fewer than 16 days in the UK this year. |

| Overseas test 2 | Not UK resident in any of the previous three tax years, and you spend fewer than 46 days in the UK this year. |

| Overseas test 3 | You work full-time overseas (averaging at least 35 hours a week, no significant breaks), spend fewer than 91 days in the UK, and work in the UK on fewer than 31 days (a workday being over 3 hours). |

| Overseas test 4 | You die in the year, were not UK resident in the previous two years, and spend fewer than 46 days in the UK. |

Sufficient ties test

If neither automatic test settles it, you weigh five ties against your UK days. The ties are: a family tie (UK-resident spouse, civil partner or minor children), an accommodation tie (UK accommodation available and used at least one night), a work tie (40 or more UK working days of 3+ hours), a 90-day tie (over 90 UK days in either of the previous two years), and a country tie (more days in the UK than any other single country, only for those resident in one of the previous three years). The number of ties needed depends on your days and whether you were recently resident. For a leaver who spends 120 days here, three ties make you resident; an arriver would need four.

Statutory Residence Test indicator

A rough guide only, based on the day-count and tie thresholds. It does not capture every rule and is not advice.

Enter your details and select Check status.

Income tax: resident, non-resident and split-year

Once UK resident you are generally taxed on your worldwide income, even if paid abroad. As a non-resident you normally pay UK tax only on UK-source income such as UK rent, UK pensions and UK company dividends. If you leave part-way through a year you may qualify for split-year treatment, so only the UK-resident portion is taxed on worldwide income.

Income tax bands, 2025/26 (England, Wales, Northern Ireland)

| Band | Taxable income | Rate |

|---|---|---|

| Personal allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

Dividend tax rates, 2025/26 (after the £500 allowance)

| Band | Rate on dividends above the allowance |

|---|---|

| Basic | 10.75% |

| Higher | 35.75% |

| Additional | 39.35% |

Dividend tax calculator

Estimates UK dividend tax after the £500 allowance. Illustrative only.

Enter an amount and select Calculate.

Split-year treatment and the eight cases

Split-year treatment is one of the most valuable reliefs when leaving or arriving mid-year. Instead of being fully resident or fully non-resident for the whole year, the year splits into two periods with different treatment. There are eight cases. The most common on leaving are Case 1 (starting full-time work overseas), Case 2 (accompanying a partner who does), and Case 3 (ceasing to have a UK home). On arrival, Case 8 (returning to the UK) is the usual one.

Case 1, starting full-time work overseas: the UK part runs from 6 April to the day before your overseas job starts, and you are non-resident from then to 5 April. You are taxed on worldwide income for the UK part and only on UK-source income afterwards, which can save substantial tax on foreign earnings. Case 3, ceasing to have a UK home: the split usually falls when you give up your UK home, relevant if you sell or end a UK tenancy before emigrating. Case 8, returning: the UK part begins when you arrive and a UK home becomes your only or main home.

Dividends from your own UK limited company

If you own a UK company and take dividends in a year where you qualify for split-year treatment, be careful with timing. A dividend paid while you are still UK resident is generally taxed in full at the UK rates above (10.75%, 35.75% or 39.35% after the £500 allowance), even within a split year, unless specific treaty relief applies or the dividend arises after you are non-resident with no continuing UK-resident company involvement. The payment date relative to your residence status is what matters, so plan dividend timing before you leave.

Capital Gains Tax and returning to the UK

CGT rates, 2025/26

| Asset type | Below the higher-rate band | Within the higher or additional band |

|---|---|---|

| Non-property assets | 18% | 24% |

| Residential property | 18% | 24% |

Temporary non-residence (return within 5 years): if you leave, become non-resident, then return within five tax years, gains you made while non-resident on assets held before departure can become UK-taxable in the year you return. For example, you leave in July 2025, sell an overseas asset in 2027, and if you return in 2028/29 you may owe UK CGT then on that gain. Beyond five years: stay non-resident for more than five tax years and gains realised while non-resident generally fall outside UK CGT, depending on the asset.

Moving to the UK: once resident again you are liable on worldwide income, and you must check the temporary non-residence rules. The new FIG regime (from 6 April 2025), for those non-resident for at least 10 years, gives relief on foreign income and gains for up to four years after returning.

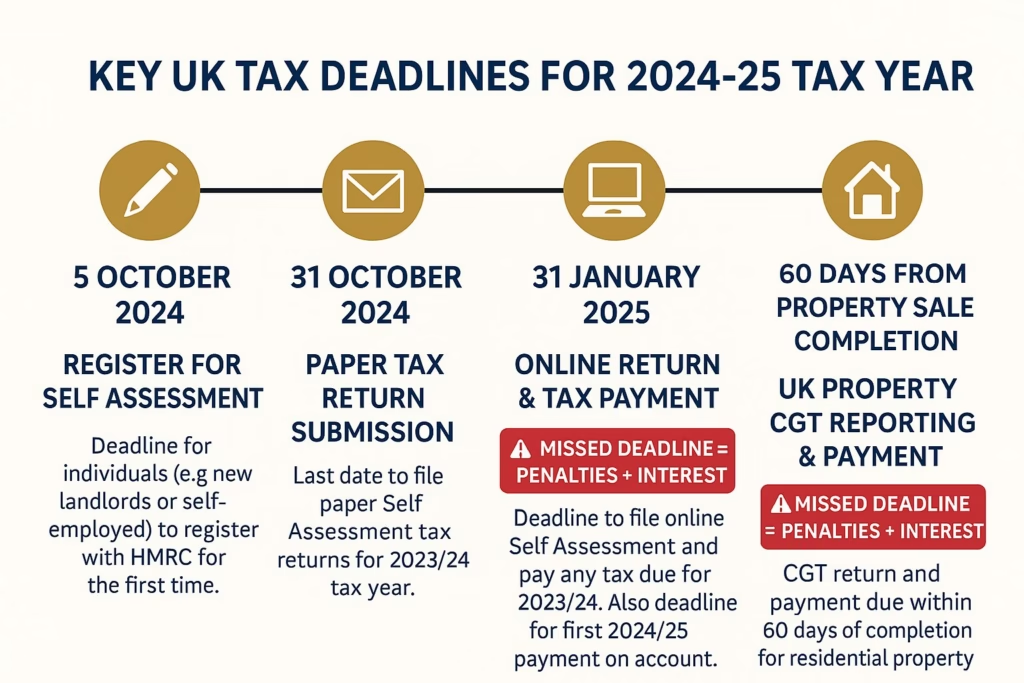

Forms, deadlines and key dates

| Item | Form / service | Deadline / notes |

|---|---|---|

| Notify HMRC of departure (no Self Assessment) | Form P85 | Submit once you leave; include P45 parts 2 and 3 if relevant. |

| Notify residence status (Self Assessment filer) | SA109 residence pages | With your SA return: paper by 31 Oct, online by 31 Jan. |

| UK tax year | – | 6 April to 5 April. |

| Return to UK, temporary non-residence CGT | – | If you return within 5 years, CGT is triggered in the year of return. |

| CGT on UK property for non-residents | CGT on UK property service | Report within 60 days of disposal. |

How to claim your tax refund: Form P85

If you have worked in the UK and are now leaving, you may be due a refund. The main route is Form P85, which tells HMRC you have left and triggers a review of your year.

Before you start, gather:

- Your P45 (parts 2 and 3) and National Insurance number.

- Your new overseas address and contact details.

- Start and end dates of your UK employment, and all UK employers in the year.

- The dates you were present in the UK during the tax year.

- Details of any UK income continuing after you leave, such as rent or pensions.

Completing Form P85 online

| Step | What to prepare | Key details | Why it matters |

|---|---|---|---|

| How to submit | Government Gateway login | Use HMRC’s online P85 service. | Fastest route; guides you through each section. |

| Personal details | ID and contact info | Name, NI number, DOB, current UK and new overseas address. | Lets HMRC verify and contact you after departure. |

| Employment information | P45(s) and employer info | Employer names, PAYE ref, leaving dates, year-to-date pay and tax. | Calculates final liability and any refund. |

| Departure details | Travel dates and destination | Exact date you left and the country you moved to. | Affects the SRT outcome and split-year treatment. |

| Future UK income | Ongoing UK sources | UK rents, pensions, company dividends after leaving. | Determines whether you still need UK returns. |

| Overseas employment | New job details | Overseas employer, role and start date. | Helps HMRC assess non-residence. |

| Bank details (refunds) | Account info | Where bank transfer refunds are available; otherwise by cheque. | Speeds up international refunds. |

| Review and keep records | Copies of everything | Check accuracy and save a copy of the P85 and evidence. | Avoids delays and supports your residence position. |

By post: download the P85, complete it in black ink and capitals, attach P45 parts 2 and 3 (keep part 1A), and send to HM Revenue and Customs, Pay As You Earn, BX9 1AS, United Kingdom, by tracked mail from overseas. Already left? You can still file, with no penalty for being late, though HMRC generally allows only four years from the end of the tax year to claim. Who should not use P85: Self Assessment filers (use the SA109 instead, though P85 can still get you an NT code), people leaving only temporarily, the self-employed or own-company directors, and students on a gap year returning within the tax year.

Leaving-the-UK refund estimator

Estimates your 2025/26 income tax on UK employment income and compares it with the tax already deducted. Illustrative only: it assumes employment income, applies the personal allowance (tapered above £100,000), and ignores National Insurance, student loans and the finer split-year apportionment, so a valid split-year claim could increase your refund further.

Enter your figures and select Estimate refund.

Refund examples

Example 1: employee leaving mid-year

Sarah worked in London from 6 April 2024 to 30 September 2024, earning £30,000 gross, then moved to Australia. On a higher-rate emergency assumption her employer deducted about £4,686. Her actual liability on £30,000 is £3,486 (£17,430 taxable at 20% after the £12,570 allowance), and split-year treatment confirms she is UK resident only to 30 September. HMRC refunded about £1,200 within eight weeks of a correctly completed P85.

Example 2: seasonal worker returning home

Marco came from Italy on 15 May 2024, earned £8,000 in hospitality, and left on 31 August 2024. As his £8,000 is within the £12,570 personal allowance, he owed no UK tax, so the £800 deducted on a temporary code was refunded in full, about ten weeks after his P85.

Example 3: returning home with split-year treatment

Priya worked in the UK for three years before returning to India on 15 October 2024 for a new role, earning £45,000 across the year. Under split-year (Case 3, ceasing to have a UK home) she is UK resident only to 14 October, with £26,250 in that period. After her £12,570 allowance, £13,680 is taxable at 20%, a liability of £2,736. Her employer had deducted about £6,486 across the year, so HMRC refunded about £3,750.

Receiving your refund

Most HMRC refunds take six to twelve weeks from a correctly completed form, longer in the January to April peak or if details do not match, you had several employers, you claim split-year, or your case is selected for checks. HMRC has been moving P85 refunds from cheque to bank transfer (from autumn 2025), which avoids the cost and delay of overseas banks cashing sterling cheques. If you close your UK account before the cheque arrives, or worry about post, you can appoint a nominee in the UK to receive and forward it, using a 64-8 authorisation for a professional agent. If a cheque has not arrived within three months of issue, contact HMRC with your reference to cancel and reissue it.

Checklist for leaving the UK

- ✓ Determine residence under the SRT: overseas tests first, then UK tests, then sufficient ties.

- ✓ If leaving mid-year, check whether split-year treatment applies.

- ✓ UK-resident period: account for income tax on salary, self-employment, interest and dividends.

- ✓ Non-resident period: UK tax only on UK-source income.

- ✓ Own-company dividends: resident status can tax the whole year even if you leave mid-year.

- ✓ Disposals while non-resident: check the 5-year temporary non-residence rule on return.

- ✓ Returning: consider the FIG regime and temporary non-residence for CGT.

- ✓ File P85 or SA109 on time, and report continuing UK-source income.

- ✓ Keep records of UK days, overseas home, work days and overseas employment.

- ✓ Take advice on treaties, non-resident landlord status, CGT and your company dividends.

Common mistakes to avoid

Waiting until after leaving to start the process

You can file Form P85 as soon as you know your departure date. Filing early means faster processing and a faster refund.

Not keeping copies of submitted forms

Processing takes months and post can go astray. Keep copies of your P85, P45 and supporting documents so you can prove submission.

Closing your UK bank account too soon

Close it before the refund arrives and you are left with slow, costly international cheques. Keep one UK account open, or appoint a nominee, until the refund or bank-transfer facility is in place.

Not notifying HMRC of address changes

If you move after filing, tell HMRC at once. Cheques sent to an old address may never arrive, and replacements add months.

Assuming you do not need to file because you are leaving

If you have UK-source income you may still need to file, and HMRC will pursue tax owed wherever you live. Formally notifying departure closes your affairs cleanly.

Overlooking split-year treatment

Split-year relief is not automatic; you must identify that you qualify and claim it. Many people overpay simply by missing it.

Forgetting the four-year claim deadline

HMRC generally allows four years from the end of the tax year to claim. Leave it too long and the right to a refund is lost, even if you overpaid by thousands.

Planning a move in or out of the UK?

Residence, split-year treatment, CGT on return and company dividends all reward early planning. Book a call to work through your position.

Frequently asked questions about UK exit taxes

What forms must I complete when leaving the UK?

If you do not file Self Assessment, complete Form P85 (with P45 parts 2 and 3). If you do, include the SA109 residence pages with your return. Tell HMRC as soon as you leave; SA deadlines are 31 October (paper) and 31 January (online).

How does HMRC decide whether I am UK tax resident?

Through the Statutory Residence Test (FA 2013 Sch 45): automatic UK tests, automatic overseas tests, then sufficient ties. Broadly you are resident if you spend 183+ days here or have a UK home, and non-resident if you work full-time abroad and spend fewer than 91 days in the UK.

What is split-year treatment?

It divides the tax year into a UK-resident part (taxed on worldwide income) and a non-resident part (taxed only on UK income). There are eight cases under RDR3, such as starting work abroad or returning to the UK.

What income stays taxable in the UK after I move abroad?

UK-source income, such as rent, pensions and dividends from UK companies. Non-resident landlords must register under the Non-Resident Landlord Scheme or have tax deducted at source.

What happens to dividends from my own UK company after I leave?

They remain UK-source income. Even with split-year treatment, dividends paid while you are UK resident are generally taxed at 10.75%, 35.75% or 39.35%, so timing relative to your residence status matters.

What are the CGT rules if I leave or return to the UK?

Non-residents pay CGT on UK property but generally not on foreign assets, unless they return within five years, which triggers the temporary non-residence rule. Rates are 18% and 24%, with a £3,000 annual exemption.

How many people leave the UK, and why does it matter for tax?

ONS data indicates hundreds of thousands emigrate each year, mainly for work, study or retirement (figures are regularly revised, so check the latest release). Many notify HMRC via P85 or SA109 to secure refunds and avoid double tax; failing to do so risks over or underpaying.

About the author: Simon Misiewicz

Simon is a senior cross-border tax adviser specialising in UK residence and non-residence for high-net-worth individuals and business owners. With over 20 years of experience advising on residence, the remittance basis and international mobility, he has authored articles for accountancy and tax journals, lectures widely to advisers and at postgraduate tax programmes, and contributes to HMRC on the technical guidance for the Statutory Residence Test and temporary non-residence rules.

This page is general information and not advice. The calculators are illustrative estimates only and do not account for every rule. Tax rules, rates, thresholds and deadlines change. Take specialist advice for your own circumstances before acting.